Export competitiveness of Sri Lanka: Role of an industrial policy

1. Introduction

The economic growth of Sri Lanka did not match the high hopes prevailed after the independence and economic liberalization in late 1977 which resulted a rapid but unsustainable growth. Economic liberalization indeed generated positive economic and demographic outcomes compared to the closed economy before 1977. The consensus is on the underperformance of economic and export growth, especially compared to fast growing economies in East Asia. Macroeconomic mismanagement, half-hearted liberalization or “unfinished agenda”, initial conditions, and unwillingness to bear the political cost of adjustment are blamed for the underperformance (Dunham and Kelegama 1995). The mismatch between the success of import liberalization and export promotion created a persisted trade deficit with slow growth of exports (Dunham and Kelegama 1995; Wijesinghe and Dissanayake 2023). The persistent trade deficit and fiscal mismanagement have led Sri Lanka to accumulate a substantial and unsustainable level of debt. In this context, there is no compelling argument against the notion that the path for a sustainable growth and recovery for Sri Lanka lies in fostering export-led economic growth. This article delves into the role of an industrial policy in achieving a sustainable export-led growth trajectory.

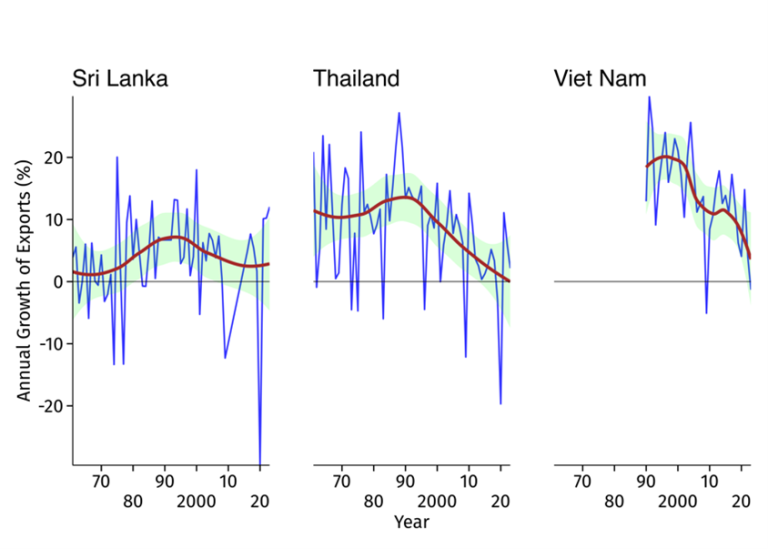

Sri Lanka’s post-liberalization growth potential was drastically reduced by its inability to maintain a high export sector growth sustainably, unlike the East Asian success stories like Thailand and Vietnam (Figure 1). A possible causal factor is the lack of diversification of the export basket, particularly in relatively complex products. As illustrated in Figure 2, Sri Lanka currently primarily produces low and medium-tech agricultural and manufacturing products. Concentrating on products like wearing apparel, tea, and rubber products limits future growth potential because these sectors have lower growth rates in the global market. Therefore, while Sri Lanka must maintain its comparative advantage in competitively produced products, it is necessary to innovate into new products leveraging current technical knowledge, comparative advantage, and global trends.

Figure 1: Annual growth rate of exports of Sri Lanka, Thailand, and Viet Nam:

Source: Author’s illustration using World Development Indicators (WDI) data

Figure 2: Product Space[1] of Sri Lanka

The high concentration of exports in textiles and apparel presents a significant challenge, particularly given the limited opportunities for innovation in producing more complex products and the declining global share of the industry. As illustrated in Figure 3, Sri Lanka’s wearing apparel exports experienced a low compound annual growth rate between 2012 and 2022, contributing to the low overall export sector’s growth rate of only 2.3%. However, there was a potentially encouraging trend during this period: the high growth rate of relatively complex products, such as electrical machinery, apparatus, and appliances. These products in HS chapter 85 recorded a trade-weighted average annual growth rate of 10%, significantly higher than the average export growth rate of Sri Lanka, which was approximately 2.5%. Furthermore, more complex products like electric sound or visual signalling apparatus experienced a substantial growth rate of 39% between 2012 and 2022. Given the current production and technological know-how, Harvard Atlas has identified semiconductors devices, electrical insulators made from various materials, electric motors, and other products in HS chapter 85 as potential new product opportunities for Sri Lanka.

Figure 3: Compound annual growth rate of exports by Sri Lanka:2012-2023 at HS-four digitsMoreover, the tightening environmental regulations in export destinations like the European Union (EU) incentivise Sri Lanka to acquire comparative advantage in environmentally sustainable products. The Carbon Border Adjustment Mechanism (CBAM) of the EU imposes a tariff on carbon-intensive exports increasing the trade cost of products covered by CBAM. Although there is no immediate risk of CBAM for Sri Lanka, as competitively exported products like textiles and wearing apparel are not under CBAM, Sri Lanka faces a risk of CBAM being expanded to similar products. Other environmental or trade regulations, such as those related to synthetic material inputs from fossil fuels or plastics, address the rising concern about microplastic pollution and the impetus for a global plastics treaty (Barrowclough & Vivas, 2021). Importantly, apparel sector is a significant contributor to microplastic pollution. Under European Green Deal, the EU is tightening regulations to reduce microplastic pollution (European Commission Directorate General for Environment, 2023).

The European Commission has proposed a targeted amendment to the Waste Framework Directive to improve the management of textile waste, aligning with the EU Strategy for Sustainable and Circular Textiles (European Commission, 2023). A provisional agreement on this revision was reached in February 2025 between the European Parliament and the Council paving way for each Member State of the EU to set up its own Extended Producer Responsibility (EPR) scheme for textile and footwear products. By taking responsibility for the end-of-life phase of their products, producers will be incentivized to create longer-lasting textiles that are easier to reuse, repair, and recycle (European Commission, 2025). Thus, Sri Lanka has an incentive to diversify production into sustainable fabric and wearing apparel. It should be noted that due to the relatedness of these new products to existing know-how, the transition will be relatively easy.

While consumer preference and regulatory scrutiny over consumer goods like apparel are growing, the net emission targets, and nationally determined contributions have incentivized countries to adopt e-mobility initiatives. National security concerns have also motivated countries like the US to supply diversification of crucial EV batteries. Production of EV battery components and recycling of EV batteries are rapidly growing markets in the EU, the US, and East Asia. Joining these growing manufacturing value chains capitalising on comparative advantage in assembly activities, infrastructure like deep seawater ports, and natural resource endowments like graphite will help Sri Lanka’s incomplete structural transformation and declining trade openness (Figures 4 and 5).

Figure 4: Incomplete structural transformation of Sri LankaSource: Author’s illustration using WDI data

Figure 5: Declining trade openness of Sri Lanka: 1960-2023

The preceding discussion highlights the need for Sri Lanka to adopt more sustainable manufacturing practices in the apparel industry due to increasing environmental regulations and opportunities in EV battery manufacturing and recycling. Given the growing focus on industrial policy, a thorough examination of its role in supporting production in these sectors is essential.

3. What is the role of industrial policy?The distortionary market interventions by the state in the era of “import substitution” naturally raises concerns over the effectiveness of industrial policies. Arguments against industrial policy emphasize that governments may struggle to identify successful industries and that policies can be captured by unproductive firms. Critics highlight several risks, including the potential failure of targeted industries, discrimination against foreign trade partners, and reduced economic dynamism due to government intervention. Industrial policy can also lead to economic distortions, where subsidies and protectionist measures create artificial advantages rather than genuine competitiveness. Additionally, concerns include subsidy races between countries, policy capture by inefficient firms, and the persistence of high tariff protection in key sectors despite deepening trade relations (Reed, 2024).

Industrial policy, despite its criticisms, can support export-led growth by strategically identifying tradable sectors with high compound growth rate in world market and comparative advantage, and addressing market failures that limit their expansion. While “picking winners” may not be possible for Sri Lanka, the risk of “picking losers” can be minimized by selecting viable industries based on trade data and global economic conditions (Reed, 2024). A sound industrial policy should consider technological relatedness to predict future comparative advantages and implement sector-specific interventions to address market constraints, rather than old-style reliance on excessive subsidies, tariff protection, and establishing government parastatals. Additionally, industrial policies can be designed to comply multilateral rules-based trade system under World Trade Organization (WTO). Table 1 shows a framework to identify more efficient and rules-based industrial policies Sri Lanka can follow.

| Protectionist industrial policy measures (Prohibited under WTO and inefficient) |

Industrial policy measures within WTO rules and more efficient |

|---|---|

| Targeted tariffs | Tariff negotiations (FTAs, RTAs) |

| Local content requirements | Product quality certification |

| Export subsidies | Programs to link firms to new customers and suppliers |

| Export prohibitions | Sector-specific infrastructure |

| Import bans (outside allowed specific circumstances) | Sector-specific skills programs |

| Industry-specific regulation | Innovation subsidies without local content or export contingencies |

| Innovation and value addition contingent on local sourcing or exports | Place-based policy |

| Source: Reed, 2024 | |

Table 2 lists possible industrial policy measures for Sri Lanka to ensure competitiveness in currently exported products like wearing apparel and to acquire new comparative advantage in sustainable apparel manufacturing and joining the EV battery value chain. Entering into new FTAs will increase Sri Lanka’s market access to fast-growing economies like Thailand and other East Asian countries. In addition, the existing Indo-Sri Lanka FTA can be improved by removing quantitative barriers, including quotas applicable to ready-made garments. Another important function of FTAs is that, as they are reciprocal, Sri Lanka will have to phase out inefficient protection given to unproductive domestic industries, gradually removing the anti-export bias in the economy. Sri Lanka signed FTAs with Singapore and Thailand which have provisions to lower tariffs up to 85% of product lines including phasing-out associated para-tariffs.

| Industrial Policy Measure | Identified policies for Sri Lanka |

|---|---|

| Tariff negotiations (FTAs, RTAs), regional collaboration, and trade facilitation | Removal of quota applicable for apparel exports under Indo-Sri Lanka FTA, bolstering trade links with East Asian countries, joining Regional Comprehensive Economic Partnership, and establishing National Single Window |

| Innovation subsidies without local content or export contingencies | Tax concessions if 20% value is domestically added [Current policy]. Lowering threshold to incentivize EV assembly and VAT exemptions for locally assembled EV, and removing royalty fees in graphite mining |

| Sector-specific infrastructure | Export processing zones |

| Sector-specific skills programs | Support for research and development in EV battery technologies through grants and partnerships |

| Product certification and traceability | Digitalization, increasing access to digital services and internet, and provision of technical support to fulfil traceability |

| Source: Author’s illustration | |

In addition, product certification and traceability are critical in exporting sustainable products under the regulatory scrutiny of leading export destinations like the EU. Digitalization, increasing access to digital services and internet, provision of technical support to fulfil traceability requirements should be priorities for Sri Lanka. For the growth of the EV battery value chain activities, removing some taxes on graphite mining including royalty fees, lowering threshold for tax concession eligibility in EV assembling, VAT exemptions for locally assembled EV, and support for research and development in EV battery technologies through grants and partnerships can be identified as sound industrial policy measures for Sri Lanka.

4. Key takeawaysSri Lanka's economic growth has lagged behind East Asian economies due to structural weaknesses, including macroeconomic mismanagement and an imbalance between import liberalization and export promotion. This has contributed to a persistent trade deficit and unsustainable debt. A major challenge is the lack of export diversification, with heavy reliance on low- and medium-tech products such as apparel, tea, and rubber, which have limited growth potential in global markets. To achieve long-term economic stability, Sri Lanka must adopt an export-led growth strategy that prioritizes diversification into more complex products and aligns with global market trends.

One promising avenue for diversification is the electrical machinery sector, where products like semiconductors, electrical insulators, and electric motors show growth potential. Additionally, tightening environmental regulations, such as the EU's Carbon Border Adjustment Mechanism (CBAM), create an opportunity for Sri Lanka to transition toward sustainable manufacturing. The country could expand its sustainable apparel sector and tap into the electric vehicle (EV) battery value chain, including production and recycling, leveraging its existing assembly activities, infrastructure, and graphite reserves. These shifts would enhance Sri Lanka’s competitiveness in high-value, future-oriented industries.

Industrial policy can support export-led growth by identifying high-potential tradable sectors and addressing market failures, but it should avoid excessive subsidies and protectionist measures. Effective policies should focus on tariff negotiations, sector-specific skills development, innovation incentives, and product quality certification. Key measures for Sri Lanka include lifting apparel export quotas under the Indo-Sri Lanka FTA, strengthening trade ties with East Asia, and fostering research and development in EV battery technologies. Additionally, ensuring product certification and traceability for sustainable exports will require greater digitalization, improved access to digital services, and technical support to meet international standards.

ReferencesBarrowclough D and Vivas D (2021). Plastic Production and Trade in Small States and SIDS: The Shift Towards a Circular Economy, International Trade Working Paper 2021/01, Commonwealth Secretariat, London.

https://thecommonwealth.org/sites/default/files/inline/ITWP%202021_01_0.pdfDunham, David, and Saman Kelegama. 1995. “Economic Reform and Governance: The Second Wave of Liberalisation in Sri Lanka, 1989-93.” ISS Working Paper Series/General Series 203:1–34.

European Commission. (2023). Factsheet: Targeted amendment of the Waste Framework Directive for textiles. Retrieved October 2023,

from https://ec.europa.eu/commission/presscorner/detail/en/fs_23_3636European Commission. (2025). Commission welcomes provisional agreement to enhance the circularity of textiles and reduce food waste [Press release]. Retrieved

from https://ec.europa.eu/commission/presscorner/detail/en/ip_25_548European Commission Directorate-General for Environment. (2023). EU action against microplastics. Publications Office of the European Union. https://data.europa.eu/doi/10.2779/917472

Reed, T. (2024). Export-Led Industrial Policy for Developing Countries: Is There a Way to Pick Winners? (No. 10902). The World Bank.

Wijesinghe, Asanka, and Chaya Dissanayake. 2023. “Finding the Narrow Corridor: Reforms for Export-Led Growth.” in Sri Lanka: State of the Economy 2023: Economic Policy Choices: From Stabilisation to Growth. Institute of Policy Studies of Sri Lanka.

Wijesinghe, A., Weerasinghe, M., and Dissanayake, C. (2024). “Trade Wars in Electric Vehicle Supply Chains: A Win for Sri Lanka’s Graphite Industry?”. No.17, International Economics Research Series, Institute of Policy Studies of Sri Lanka